Fannie Mae Says Mortgage Rates Could Hit 5.7% by Year End. Here's What First-Time DFW Buyers Should Know.

Key Takeaways

Fannie Mae's March forecast projects the 30-year fixed mortgage rate dropping to 5.7% by Q4 2026, which would mark the first decline in monthly payments since 2020.

The same report expects single-family housing starts to fall 6.2% year over year for most of the year, meaning fewer new homes entering the market.

The national housing supply gap just crossed 4 million homes, a deficit that would take about seven years to close even under the most optimistic building scenario.

In DFW, inventory is up over 12% from last year and median home prices are down about 2.2%, giving first-time buyers more room to negotiate than they've had in years.

The forecast was built on data from before the Middle East conflict escalated, and rates have moved higher since, so the timeline carries real uncertainty.

What Fannie Mae Is Actually Projecting

Fannie Mae released its March 2026 Housing Forecast in early April, and the headline number got a lot of attention. The agency projects the average 30-year fixed mortgage rate declining from 6% in Q1 to 5.9% in Q2, 5.8% in Q3, and 5.7% by the fourth quarter of 2026. Rates are expected to stay between 5.6% and 5.7% through 2027.

That's a noticeable improvement from their February outlook, which had rates staying at 6.1% through the first half of 2026 and holding at 6% through 2027.

Why the revision? Fannie Mae's March Economic Forecast predicts slower GDP growth than it did a month earlier. Mortgage rates tend to follow the economy's direction, dropping when growth cools. The agency also lowered its forecast for the 10-year Treasury yield, which is the benchmark that 30-year mortgage rates track most closely.

So the good news (lower rates) is partly a reflection of less cheerful news (a slowing economy). Both things can be true at the same time.

Where Rates Actually Sit Right Now

Forecasts are one thing. What you'd actually get quoted today is another.

As of April 14, 2026, the average 30-year fixed purchase rate is about 6.16%, according to Zillow. Freddie Mac's most recent weekly survey put the average at 6.37% as of April 9, down from 6.46% the week before.

Those numbers are lower than where we were a year ago. At this time in 2025, the 30-year rate averaged 6.62%. So there's been real improvement, even if it doesn't always feel like it.

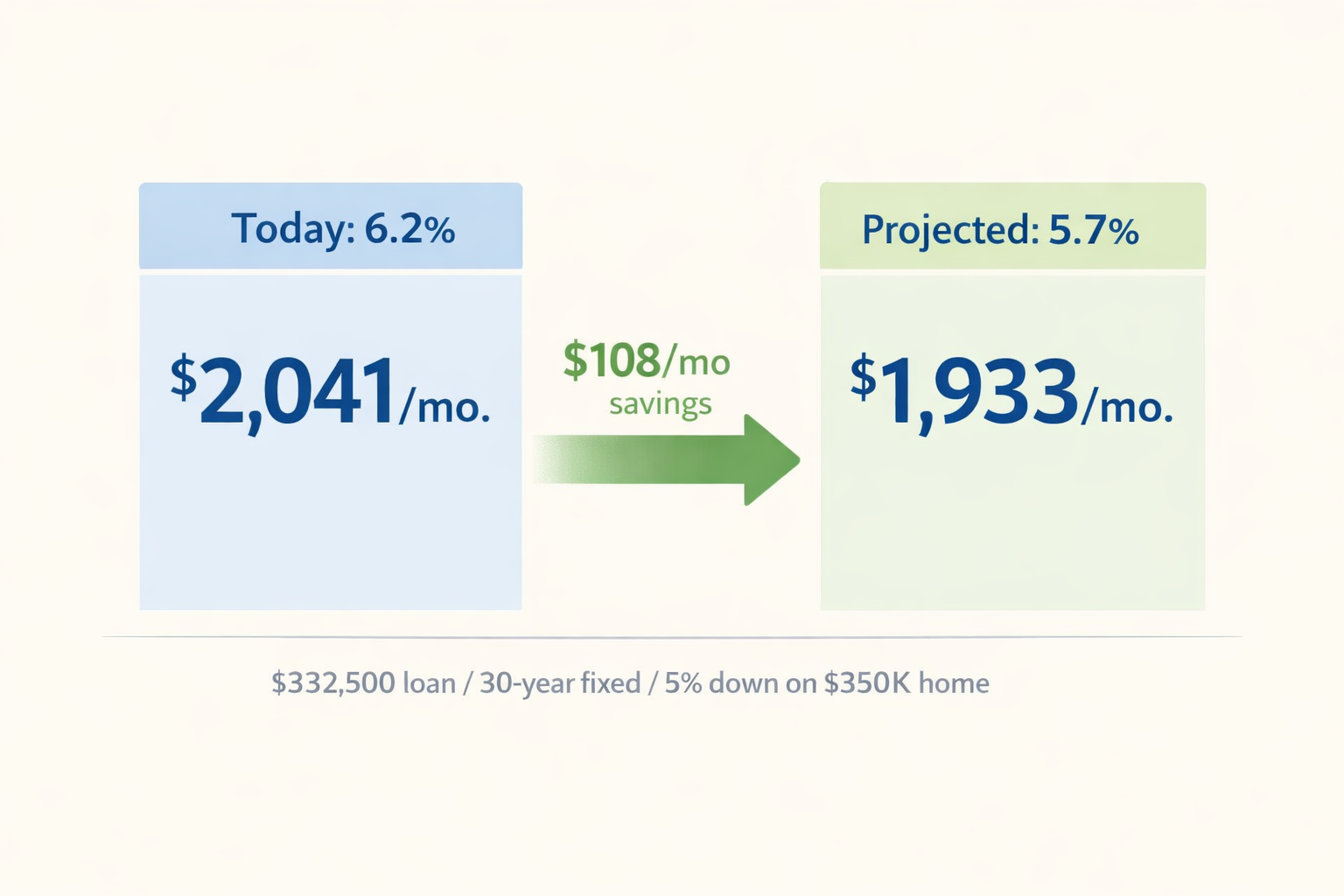

For a first-time buyer looking at a $350,000 home with 5% down (roughly a $332,500 loan), the difference between today's rate and Fannie Mae's projected 5.7% rate works out to about $100 to $110 per month. Over 30 years, that's somewhere around $36,000 to $40,000 in interest. Real money, but not the kind of gap that necessarily justifies waiting if the right home is available now.

(I say "necessarily" because there's a flip side to waiting. More on that in a second.)

The Supply Side: This Is the Part That Doesn't Get Enough Attention

The rate forecast dominated the headlines. But buried in the same Fannie Mae report is a second projection that matters just as much for first-time buyers.

Fannie Mae downgraded its expectations for new home construction, projecting single-family housing starts will decrease 6.2% year over year for the first three quarters of 2026. That's a significant drop from what they projected just a month earlier.

Zoom out, and the picture gets sharper. Realtor.com's 2026 Housing Supply Gap Report puts the national housing shortage at an estimated 4.03 million homes, up from 3.8 million in 2024. Four million. That's roughly the number of homes in the entire Chicago metro area.

Even under a scenario where construction jumps 50% above current levels, it would take approximately seven years to close the gap. And nobody is expecting a 50% jump.

Single-family starts fell to about 940,000 units in 2025, the lowest level since 2019. Tariff uncertainty is adding further friction, with construction permits and starts both declining as builders exercise caution during a period of economic volatility.

The relationship between rates and supply is worth understanding if you're buying your first home. When rates drop, more buyers enter the market. When fewer homes are being built at the same time, those buyers are competing for a smaller pool. That competition tends to push prices up. So the monthly payment savings from a lower rate can get partially eaten by a higher purchase price.

That's not a reason to panic. It's just context that makes the "should I wait for lower rates?" question more complicated than it looks.

What the DFW Market Looks Like Right Now for First-Time Buyers

If you're searching in Collin County or the northern DFW suburbs, the current numbers are worth a close look.

According to the Texas Real Estate Research Center, active inventory in the DFW area was 12.5% higher in January 2026 than a year earlier. Price softening in DFW persisted through January, marking the 11th consecutive month of year-over-year declines.

The median price for residential homes in the DFW metroplex was $385,000 in February 2026, down 2.2% year over year. Homes are averaging 61 to 71 days on market, which is a very different environment than the bidding-war frenzy of 2021 and 2022.

For first-time buyers, the practical effect is more time to think, more room to negotiate, and more sellers willing to offer concessions. Rate buydowns, closing cost credits, and home warranties are all on the table in ways they simply weren't two or three years ago.

One thing to keep in mind: the market behaves differently depending on where you're looking. Starter and mid-tier homes in the Dallas-Plano-Irving area saw price declines of over 3%, while the luxury segment posted a 3.5% gain. The growth corridor north of McKinney, including Anna, Celina, and Prosper, tends to follow its own pattern based on new construction activity and builder incentives.

The Caveat That Matters

I want to flag something that I think gets glossed over too quickly.

Fannie Mae's March rate forecast is based on interest rate data from February 27. That was the day before the U.S. and Israel launched military strikes against Iran. Since the conflict began, mortgage rates have increased.

The average 30-year rate had dropped to just under 6% in late February, its lowest level in over three and a half years. By early April, it had climbed to 6.46%. It's since pulled back again, but the swings have been significant.

Most industry groups other than Fannie Mae believe that 30-year fixed rates will stay above 6% for the foreseeable future. The MBA projects a more conservative range near 6.0% to 6.2%, and NAR projects rates landing around 6.0%.

The honest answer is: nobody knows exactly where rates land by December. The Fannie Mae projection is one credible scenario. It's not a guarantee. The geopolitical situation, inflation data, and Fed decisions between now and then will determine the actual path.

Not All Forecasters Agree

It's worth noting that the 5.7% projection is the most optimistic among the major forecasting groups.

The Mortgage Bankers Association projects the 30-year rate staying between 6.0% and 6.2% through 2026. NAR expects rates at approximately 6.0%. Fannie Mae is the only major research group calling for sub-6% mortgage rates in the near term.

That doesn't make them wrong. It means the range of credible outcomes runs from "modest improvement" to "meaningful improvement," and where we actually land depends on factors that are genuinely difficult to predict right now.

So Here's What This Means for You

If you're a first-time buyer in the DFW area, the combination of factors right now is worth paying attention to. Rates are lower than a year ago, inventory is higher than it's been in years, and sellers are offering concessions that weren't available during the frenzy years. Whether rates ultimately reach 5.7% or settle closer to 6%, the current market conditions give first-time buyers something that's been in short supply for a while: time and options. The question isn't really "will rates go lower?" It's "what will the market look like when they do?"

FAQ

-

Fannie Mae projects the 30-year fixed rate reaching 5.7% by Q4 2026, but they're the most optimistic among major forecasters. The MBA and NAR both project rates staying at or near 6%. Geopolitical events have added uncertainty since the forecast was issued, so the actual path could differ from all three projections.

-

On a $332,500 loan (roughly a $350,000 home with 5% down), the difference between 6.2% and 5.7% is about $100 to $110 per month, or approximately $36,000 to $40,000 in total interest over 30 years. Meaningful savings, but worth weighing against potential home price increases if you wait.

-

It's moving in that direction. Inventory is up over 12% year over year, homes are sitting 60 to 70 days on average, and median prices are down about 2.2%. First-time buyers have more negotiating leverage now than at any point since before the pandemic.

-

Builders face a combination of headwinds: higher material costs, labor shortages, permitting delays, tariff uncertainty, and elevated financing costs. Even though demand remains strong, these constraints are making it harder and more expensive to start new projects.

-

There's no universal answer, but the historical pattern is worth considering. Lower rates tend to bring more buyers into the market, which increases competition and can push prices higher. Many buyers who waited during previous cycles ended up paying more for the home itself. A common approach is to buy when the market conditions favor negotiation and plan to refinance if rates drop.

-

Texas offers several programs, including the Texas State Affordable Housing Corporation (TSAHC) and Texas Department of Housing and Community Affairs (TDHCA) programs, which offer down payment assistance and below-market rates for qualifying buyers. Eligibility depends on income, credit score, and purchase price. A conversation with a lender who specializes in these programs is the best first step.

I work with many lenders who are fantastic at what they do. Reach out to me at the number at the bottom of the page. I’ll get you connected for free.

Conclusion

The rate outlook is heading in the right direction, and the DFW market has more room for first-time buyers than it has in years. Both sides of the equation, rates and supply, carry uncertainty. But understanding the full picture is what separates informed decisions from reactive ones.

What's your read on the rate forecast? Are you planning to buy this year or waiting it out?

Sources

Fannie Mae March 2026 Housing Forecast, via Benzinga/Yahoo Finance (April 5, 2026) LINK

Freddie Mac Primary Mortgage Market Survey, April 9, 2026 LINK

Yahoo Finance / Zillow mortgage rate data, April 14, 2026 LINK

Realtor.com 2026 Housing Supply Gap Report (March 2026) LINK

Texas Real Estate Research Center, Texas Housing Insight, March 2026 LINK

CultureMap Fort Worth / AP, "DFW Housing Market Tilts to Buyers" (April 9, 2026) LINK

Home Buying Institute, Dallas Real Estate Market Forecast (updated February 2026) LINK

RealEstateNews.com, "Tariffs on Track to Exacerbate US Housing Shortage" (April 8, 2026) LINK

M/I Homes Dallas Housing Market Update (January 2026) LINK

Mortgage Rate Predictions 2026, The Advantage Lending (April 2026) LINK

U.S. News 2026 Mortgage Rate Forecast LINK

NAHB 2026 Housing Outlook (February 2026) LINK